According to the Federal Trade Commission, consumers reported losing more than $3.3 billion to fraud in 2020, an increase of $1.5 billion since 2019. Contributing to this uptick in fraud is the constantly expanding usage of technology in the finance industry. While technology has allowed for easier methods of digital payments and transactions, it has also created opportunities for an increase in frauds, scams, and phishing. As a result, companies have started focusing on ways to mitigate vulnerabilities within payment systems.

A study by VynZ Research states that the global fraud detection and prevention market is expected to reach $85.3 billion by 2025. One of the strategies companies are employing to tackle this problem is detecting fraud via machine learning. Machine Learning is a branch of Artificial Intelligence (AI) where computer algorithms (ml algorithms) improve and “learn” automatically through the use of training data. These models can then be used to make predictions or decisions about new datasets.

A study by VynZ Research states that the global fraud detection and prevention market is expected to reach $85.3 billion by 2025. One of the strategies companies are employing to tackle this problem is detecting fraud via machine learning. Machine Learning is a branch of Artificial Intelligence (AI) where computer algorithms (ml algorithms) improve and “learn” automatically through the use of training data. These models can then be used to make predictions or decisions about new datasets.

Benefits of Machine Learning in Fraud Detection

Machine learning for fraud detection works by analyzing consumers’ current patterns and transaction methods. It can analyze these behaviors faster and more efficient than any human analysis and as a result, it can quickly identify if there is a deviation from normal behavior. This allows for opportunities in real-time approval by the user before a transaction can be complete.

Machine learning also has the benefit of increased accuracy since human error in recording or analyzing data is eliminated from the equation. Furthermore, better predictions can be achieved since machine learning models are able to process massive amounts of data. The more data supplied to a model the more the model has to learn from and can create even better predictions.

Finally, machine learning is a fairly cost-effective detection technique for companies. Data can be analyzed in milliseconds and team members aren’t burdened with manual review and checks every time new data is acquired.

Fraud Detection Applications in Machine Learning

One common fraud technique is email phishing; a method in which an individual tries to con the recipient into responding with personal data which can then be used to access accounts. Machine Learning models have the ability to differentiate between actual and spam email addresses by analyzing the components of an email then classifying them either as good or fraudulent.

Credit card theft and payment fraud are two other techniques in which the fraudsters use stolen information to make transactions, normally where the physical card is not required, such as online payments. Machine learning models can help prevent these cases by analyzing past actions of the customer including purchase amounts, location, and purchase types and flag a transaction that seems abnormal.

Fake applications and document forgery can also result in the creation of credit cards and accounts tied to the victim, who is then responsible for the payments. Neural network models can be trained to differentiate between these fake identities and require approval before the application is accepted.

Keys to Successful Implementation of Machine Learning in Fraud Detection

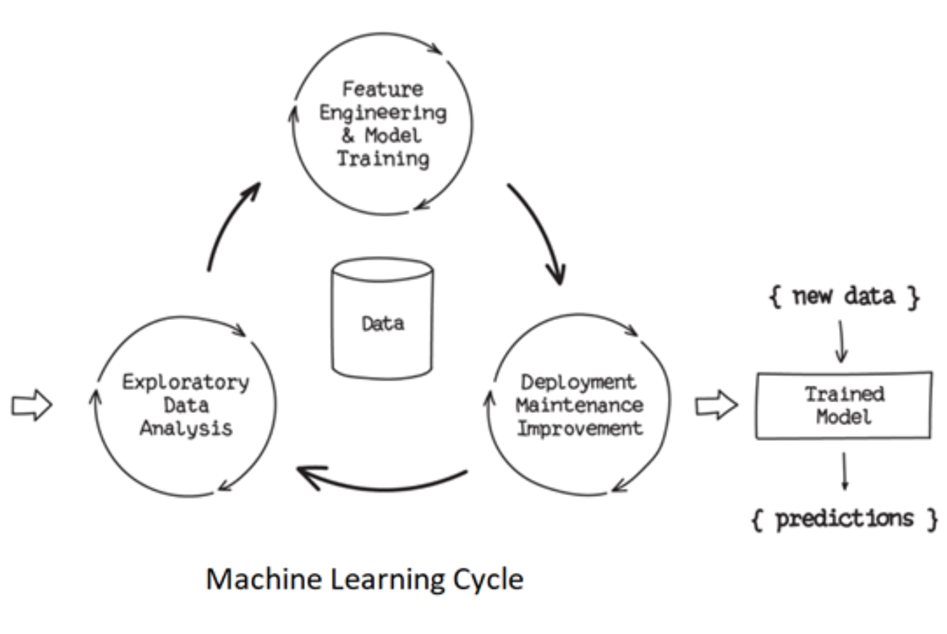

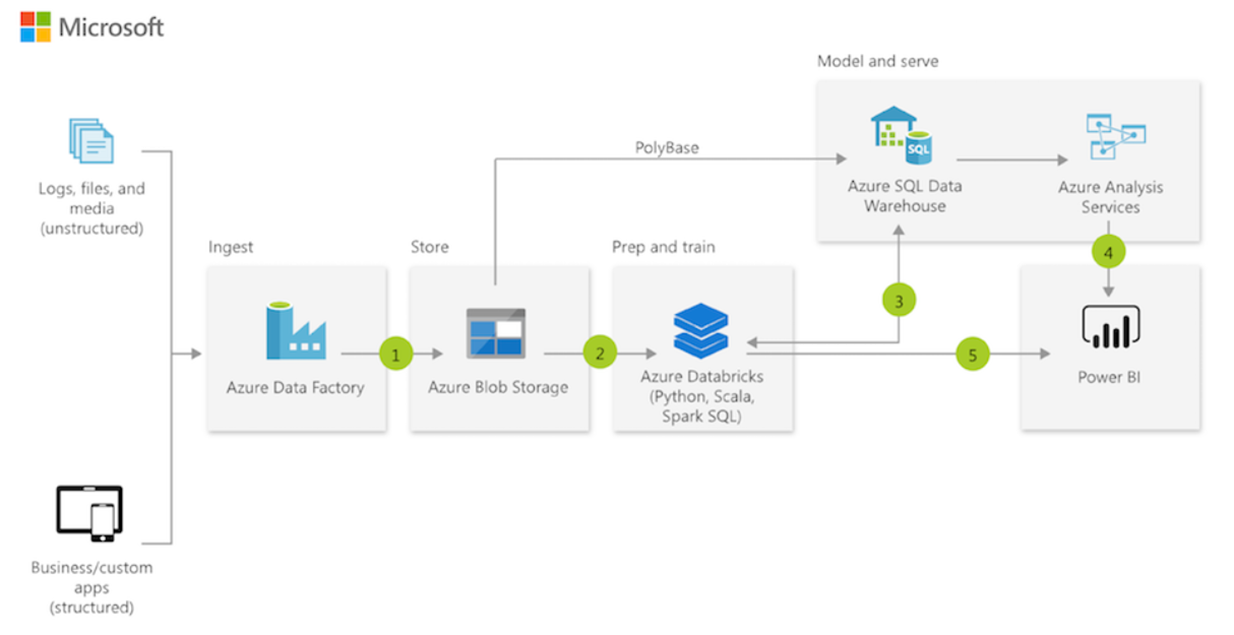

While machine learning can save consumers and businesses exponential amounts of time and money when implemented correctly, it can come with some initial startup challenges. The key to any accurate machine learning model is the input data. Not only does enough historical data need to exist for the model to derive an accurate representation but the data also needs to be accessible. If transaction information, consumer details, and purchase activities are dispersed among detached data sources, getting the data in a viable format for modeling could be difficult. A remedy for this would be to implement a modern data platform, as in the Azure example below:

Another challenge involves business level decisions. For some machine learning models historical cases need to be labeled as either fraudulent or non-fraudulent in order for the model to make predictions about new data. Creating these labels requires either sets of well-defined business rules or actual consumer feedback about whether the transaction was fake. Once a machine learning model is trained and ready for deployment, decisions also have to be made about how the predictions will be implemented in real-world scenarios. These challenges can usually be alleviated by having discussions with subject matter experts and business leaders to devise a clear path for operations.

Overall, machine learning can be an invaluable tool in the detection and prevention of fraud. It can help businesses provide a more secure platform for their customers and provide customers with the confidence to continue reaping the benefits of technology in the financial sector. Through well-designed data models and coherent business rules, implementing fraud detection via machine learning can be straightforward and time saving. In the video below, we will demonstration a Financial Fraud Detection Notebook from Databricks. This notebook uses a synthetic dataset to illustrate the process of conducting a machine learning model.

More Information

3Cloud offers a variety of resources to help you learn how you can leverage Modern Data Analytics. We also offer events such as:

Contact us directly to see how we can help you explore your about modern data analytics options and accelerate your business value.